Our Lawyers Get Your Long-Term Disability Benefits Paid

98% percent of our clients collect disability insurance benefits. We have helped thousands of disability insurance claimants throughout the USA to collect hundreds of millions of dollars of disability insurance benefits. Thank you for considering our law firm to help you.

You can greatly increase your chances of long term disability insurance benefit approval by learning all about the claim handling tactics of your disability insurance company.

Discover How Your Disabling Condition Should be Presented to Your Disability Company

Disability insurance companies always argue that diagnosis does not equal disability. Proving that your medical condition is disabling is the most challenging aspect of any long term disability insurance claim.

Explore How Disability Companies Evaluate Your Occupation

Disability insurance companies are notorious for minimizing your occupational duties. This technique is used as a tool to prove that you can perform duties which differ from the job you actually performed while working.

Knowledge is Power. Learn Everything About Disability Insurance Claims

We hope you enjoy these great resources and we invite you to ask our disability insurance lawyer any questions or to leave a review about your experience with your disability insurance company

Established in 1979, we are a national disability insurance law firm that helps individuals collect disability insurance benefits. We have helped thousands of claimants throughout the USA collect over $800 million in disability benefits and we know exactly what it takes to get your benefits paid. We welcome you to contact us for a free phone consultation with one of our disability insurance lawyers.

Understanding Disability Insurance & Choosing the Right Policy

Disability insurance also known as disability income insurance is an insurance product that will pay a monthly benefit amount if you are unable to work.

Disability Income Insurance should not be confused with Social Security Disability Benefits, which are extremely difficult to get approved and limited in the amount of money paid each month. Social security disability is often inadequate in replacing your income if you cannot work, therefore every person that works should make sure they have a long-term disability insurance policy.

Most disability insurance policies will cover up to 66% of your annual pre-disability work earnings and if the disability insurance company approves your claim, then benefits are paid monthly.

Disability insurance is sold by more than 40 different insurance companies and each company offers different policy language and different pricing. The monthly premium for disability insurance will vary based on more than 30 factors with the most common being the amount of your monthly benefit, your age at time of obtaining coverage, duration of time that benefits will pay, your definition of “disability”, and whether your policy is an individual or employer provided disability policy. Short and long-term disability insurance claims are paid with high frequency, but you must be diligent in order to protect your monthly benefit on an ongoing basis. Every employee should have disability insurance in order to protect themselves and their family financially.

According to the Social Security Administration Disability Probability Tables For Insureds Born in 1997 more than 27% of employees will be unable to work for at least 12 months or more before reaching retirement age. Despite the high likelihood of being unable to work most people either never purchase disability insurance or are unaware of its existence.

As disability insurance lawyers that have helped thousands of people nationwide to get paid disability income benefits, this article will educate you about the different types of disability insurance policies and help you to buy the best disability insurance policy possible.

What are the different types of Disability Insurance Policies?

There are multiple types of disability insurance policies, because unlike life insurance which only pays if the insured dies, disability insurance policies are often 20 pages long and have numerous options available. Disability insurance policies usually contain language that is not easy to understand and when buying a disability income policy it’s hard to understand the applicability of each disability policy provision. Most consumers are unaware of the state and federal laws that will apply to a disability policy depending upon whether your disability policy is either purchased through your employer or on your own from an insurance agent. You want to make sure you buy a disability insurance policy that will truly pay benefits and that you have the best legal remedies available should your short or long term disability benefit claim be denied.

Buying a disability insurance policy is similar to shopping for a computer that is offered with lots of different options. Most consumers don’t fully understand the different available options and you don’t really know if you will need all of the available options. The more favorable terms and language in your disability policy, the more it is going to cost.

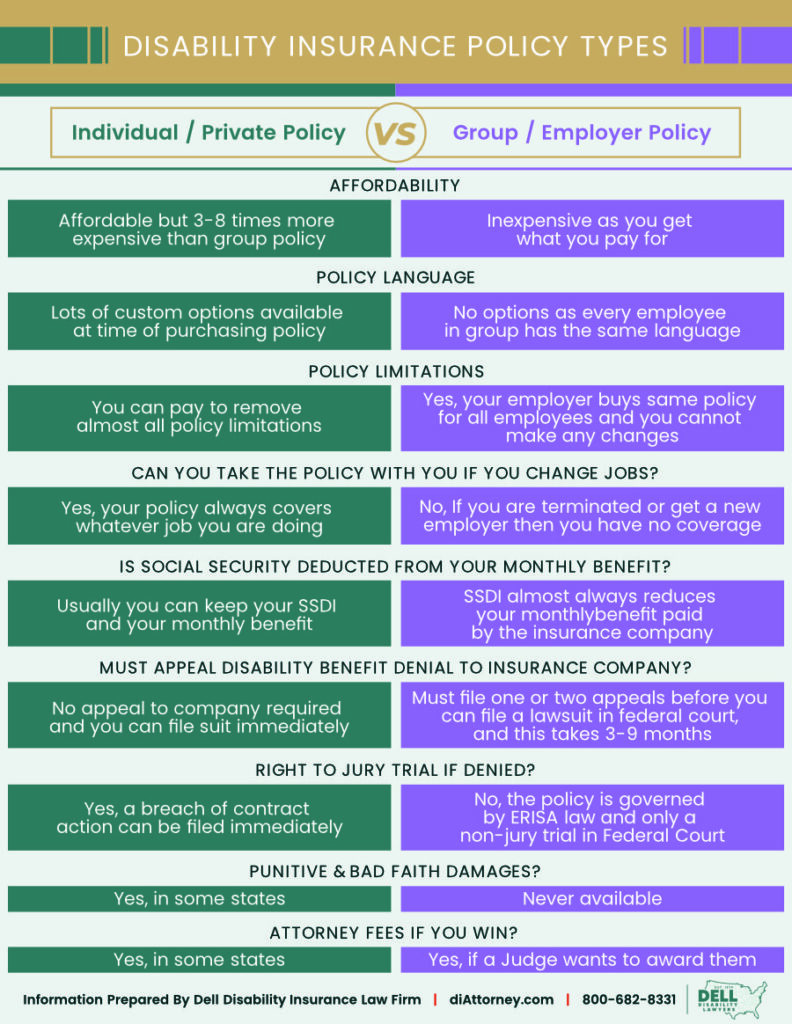

We classify disability insurance policies into two types:

Individual / Private disability income policy

Group / Employer provided disability income policy

An individual disability policy is one that you buy from an agent that sells a custom designed disability policy to meet your needs and the premium will vary greatly based upon your age, prior medical history, type of work you perform and the options you decide to include in your policy. An individual disability policy is a contract between you and your disability company that will continue regardless of who you work for or what type of work you do.

With a Group / Employer disability policy, your employer negotiates one policy with the long-term disability insurance company, and almost every employee in your company has the same disability policy with the same terms and conditions. Group disability insurance offered by an employer is very similar to Group Health insurance in the sense that there are very few options and it’s a take it or leave it situation. Some employers pay the premiums as an employee benefit and others allow the employee to pay the premiums if they want the employer provided disability. If you are either terminated or take a new job without being considered disabled, then your group/ employer disability policy will no longer cover you.

What is the difference between an Individual and a Group / Employer Provided Disability Income Policy?

There are significant differences between Individual and Group disability insurance policies and in the chart below Dell Disability Lawyers have created a comparison chart to highlight the major differences. Individual / Private disability insurance policies are far superior to a Group Disability insurance policy, but they often cost 8-10 times as much per every $1,000 of monthly benefit.

At www.diattorney.com, you can search for extensive information about how each disability company will act when it comes time to collect disability insurance benefits. If you have any disability insurance questions you can ask our disability lawyers a question and we usually answer the same day.

Where can you buy a Disability Insurance Policy?

A disability insurance policy can be purchased directly from an insurance company, an association that you may be a member of, or most commonly it’s offered as a benefit by your employer. There are more than 40 different disability insurance companies that sell disability insurance and every company sells a different type of disability income policy. Whether you are an individual seeking to buy a private disability insurance policy or a company seeking to buy a group disability insurance for your employees, it is important to work with an insurance agent that specializes in long term disability insurance. Dell Disability Lawyers doesn’t sell disability insurance but you can contact us for salesperson recommendations based upon our experience of working with some of the top disability insurance sales people in the country.

Who are the 20 largest disability insurance companies by LTD Premium Collection?

As you would suspect some disability insurance companies are better than others and you can learn about each of the disability insurance companies by reading disability insurance company reviews. According to Ibisworld.com, the disability insurance in 2020 was estimated at $19 billion dollars in short and long term disability premiums and a majority of the disability insurance policies sold were employer provided group disability insurance policies. According to Milliman’s 2020 US Group Disability Insurance Market Study the top highest grossing companies for long term disability insurance premiums were:

What type of Disability Insurance Policy should you buy?

The answer to this question is not clear cut because every individual has a different set of circumstances that makes their needs unique. Generally, individual / private disability policies are the most desirable because you can buy a true “own-occupation” definition of disability that pays disability insurance benefits if you are unable to perform the duties your occupation. With an own occupation definition that lasts for the duration of your policy, you can be paid 100% of your benefits even if you can perform a different occupation that requires a different set of skills.

Most group disability policies offer an own-occupation definition of disability but it usually only last for 24 months and the definition of own occupation is how your occupation was performed in the national economy and not how you actually performed your job. For people with pre-existing conditions, a private policy will usually exclude those conditions, but a group disability policy will not exclude pre-existing conditions as long as you work and have your policy for at least 12 months prior to your date of disability.

A group disability policy is a fraction of the cost of an individual policy which is why many people prefer group over individual. The problem with a group / employer provided disability policy is that it is subject to the Federal law of ERISA. ERISA is a horrible law that protects insurance companies and limits the rights of individuals that have group insurance policies such as disability or health insurance.

With a private disability insurance policy you have the right to sue the disability company and you will get a jury to determine your eligibility. You also have the right in some states to seek bad faith and punitive damages for refusing to pay disability benefits. In a group disability policy if you are denied you must appeal to your disability insurance company and then if you lose the appeal you can only file a lawsuit in federal court. Your group disability denial will be decided by a Judge and often the Judge is limited to determining not whether you are disabled, but rather did the insurance company act reasonably in reviewing your disability insuranceclaim. If the Judge thinks you are disabled, but also finds the insurance company acted reasonably in reviewing your claim, then you lose and get nothing.

Further, with a group ERISA governed disability policy, the judge can never award punitive or bad faith damages. An award of attorney fees is possible with both a group and an individual disability policy. The inability to take a group disability policy with you when you change employers is a major disadvantage. There is no guarantee your next employer will offer long term disability insurance and if you have a pre-existing condition then you cannot buy a new policy to cover the pre-existing condition.

There are many pro and cons of private versus group disability insurance policies that must be considered. There are some good group disability insurance policies, but unfortunately most employers don’t have the knowledge to buy a policy that provides the most protection for their employees.

If you can afford it then you can never go wrong with an individual disability insurance policy. Make your selection wisely as every disability insurance company is different and even though the prices may be similar you should investigate the reputation and reviews of each disability insurance company when it comes time to get paid benefits.

Reviewed by Bryan on January 23rd 2026 Verified Policyholder | December 2025 date of disability

They don't answer or return calls... lack of communication... unorganized... takes 3-4 weeks after approval to recieve a check... they mail checks on a friday... mailed me... read more >

Reviewed by Jim on January 7th 2026 Verified Policyholder | October 2025 date of disability

From the very start they have not tried to work with me at all. So I went out for a knee surgery and it took a month and a half to get my first check. When I had turned al... read more >

Reviewed by AT&T employee on December 16th 2025 Verified Policyholder | September 2024 date of disability

They're absolutely terrible! Here you are on disability and they delay the whole process. Hold you accountable for your company's deadlines, meanwhile they will take well ... read more >

Reviewed by Tesha on December 16th 2025 Verified Policyholder | August 2025 date of disability

I’ve been dealing with Sedgwick since August 2025 for my mental health claim. They originally denied my claim even though the psychiatrist recommended that I not return ... read more >

Reviewed by Tryan on December 16th 2025 Verified Policyholder | September 2025 date of disability

Originally they approved my disability but even though my drs note and follow up info said if be out til at least the 24th of November this adjuster stopped my payments on... read more >

Reviewed by Ann on December 16th 2025 Verified Policyholder | September 2025 date of disability

LF has no sense of urgency for people without money to buy food, pay rent, etc. They take their sweet time and it's almost like they enjoy it. I have an appeal pending for... read more >

Reviewed by SC on December 16th 2025 Verified Policyholder | August 2025 date of disability

FMLA denial after Dr. who specializes in my syndromes submitted proper medical records and forms. I have Ehlers-Danlos Syndrome hEDS, hyperadrenergic POTS and a miriad of ... read more >

When it comes to securing your disability insurance benefits, it's vitally important that your disability insurance lawyer thoroughly understands the symptoms and impact of your disabling condition. Doctors can help you create strong medical records, but they're not accustomed to dealing with the rigorous documentation disability insurance companies require. Lea... Read More >

If you're seeking long term disability benefits from an insurance company, you may be concerned that you're facing an uphill battle. Fortunately, the stronger your medical evidence, the greater the odds that your claim will be approved. On the other side of the coin, one of the most common reasons for denial of long term disability benefits involves too-weak med... Read More >

When you're seeking disability insurance benefits, your medical records and treating physician's statement are two of the most important components of your claim. But because the insurance company has a vested interest in denying your disability insurance claim, it often will rely on tactics like ambushing your doctor with a phone call in an attempt to get them ... Read More >

One thing many disability insurance claimants don't know about (or expect) from the claims review process involves video and social media surveillance. Disability insurance carriers often hire people to follow claimants around with a telephoto lens - or even send social media friend requests from fake accounts - to glean whatever information they can about the c... Read More >

Getting a denial letter from your disability insurance company is one of the ultimate insults. You are sick and not able to work, yet your disability insurance company is telling you to return to work. The disability insurance company has denied your disability benefit claim and is basically calling you a liar. When receiving a disability denial letter or a ph... Read More >

One of the top reasons for terminating a claimant's long term disability benefits involves the change in the disability insurance policy's definition of "disability." This definition change often happens in conjunction with a vocational review, or an analysis of a claimant's medical records that tells the insurance company which jobs the claimant should be able ... Read More >

At Dell Disability Lawyers, we've seen insurance companies give countless reasons to deny long term disability benefits. However, most disability benefit denials tend to fall into one of a few categories - and one of the biggest ones is the paper review and independent medical exam (IME). Learn more about what this review process entails and what your claim file... Read More >

At Dell Disability Lawyers we’ve handled hundreds of long term disability insurance claims against Reliance Standard, and have learned a few things in the process. When you’re experiencing an injury or illness that makes it difficult (or impossible) to work, it can be tempting to file a claim as quickly as possible – but unless a claimant has all their ducks in a row, this could actually delay the ultima... Read More >

This case is crazy because Reliance Standard denied long term disability benefits four times in a 24 month period and forced the claimant to file four separate appeals. Our client was an insurance agent for Florida Farm Bureau Insurance Companies. In 2017 and 2018 he was forced to reduce his work hours due to pain and complications caused by peripheral neuropat... Read More >

Our client, a former Coordinator of Rehabilitation Services suffering from a multitude of chronic pain conditions, was denied long term disability benefits by Lincoln during her transition from short term to long term disability. Despite having determined our client to be disabled during the short-term disability period, in denying long term disability benefits ... Read More >

Our client was employed with the State of Oregon as a Technical Support Representative. She sought disability through her employer provider LTD Policy with Standard due to low back, hip, and lower extremity pain. She had two hip, two knee and three back surgeries.After paying her for 1.5 years Standard hired a board-certified neurologist to perform a review ... Read More >

We represent a 57 year-old claimant who’s occupation was selling commercial vehicles for many years. Her job was very physical as it required her to climb in and out of semi-trucks multiple times a day as well as operate them which was very strenuous. She went out of work in due to ongoing and severe debilitating right hip, low back, and bilateral knee pain... Read More >

Our client, a registered nurse for Dignity Health, found herself in a difficult situation after being diagnosed with lumbar spondylosis and left knee arthritis. She continued to work, however, struggled while attempting to work through chronic lower back pain and left lower extremity radicular symptoms on a daily basis. Sadly, her condition failed to improve and... Read More >

The claimant is an 64 year old former Corporate Attorney and at a prominent Florida business law firm who was forced to cease working in his highly successful and rewarding profession, job, and career on January 27, 2021, and to seek disability compensation under his policies with Lincoln due to severe symptomatology stemming from or following a viral COVID-19 i... Read More >

Unum unjustly terminated our client’s disability insurance claim after it had approved and accepted liability for six months. Unum unreasonably concluded, without any evidence of improvement, that the claimant had resumed the sustained work capacity to perform the material and substantial duties of her high level occupation as a Transportation Division Manage... Read More >

The claimant is a 58-year-old former MRI Technologist for Fairview Health Services who has long suffered from the debilitating effects of her chronic medical conditions. She has a history of neck pain as well as right arm pain and numbness dating back to 2005 with a reoccurrence of severe symptomatology in 2013. MRI of her cervical spine performed in August of ... Read More >

In the case of Amy Wright v. Reliance Standard Life Insurance Company (Reliance), Plaintiff was the vice-president of health information services at Integrity Health Care when she stopped working on August 7, 2017. She brought claims for benefits under an LTD insurance policy and a waiver of premiums under a life insurance policy.In order to be approved for LTD benefits, Plaintiff ... Read More >

This Unum lawsuit and appeal in federal court is a great victory for all Unum disability claimants. This case supports all claimants that are disabled and claim that they cannot return to work as the requirements of their job will aggravate their symptoms and make them unable to work.Mark was a personal injury litigation attorney, when he began struggling with symptoms of... Read More >

The signing of a severance package when leaving a job is not uncommon, but you may be signing away your right to pursue either a short or long term disability insurance claim. A recent lawsuit decision from the Federal Court in New York is a sad result for a SunLife policy holder that waived her right to challenge a SunLife disability benefit denial. This claim ... Read More >

In the recent case of Ferrin v. Aetna Life Ins. Co. a federal judge from the Northern District of Illinois determined that Aetna improperly terminated Ferrin’s claim for long term disability benefits and ordered Aetna to reinstate Ferrin’s claim and pay all past due benefits with interest. Prior to filing for long term disability Ferrin was an employee of Southwest Airlines. In 2008, while at work, she suf... Read More >

In ERISA cases filed in a district court asking for judicial review of a plan administrator's denial of benefits, the court is generally limited to considering only the administrative record that was before the plan administrator. The case of Robert Stallings v. The Proctor & Gamble Disability, Committee, et al., is an example of how plaintiffs with cases filed in a District Court that is under the jurisdi... Read More >

Companion Life tried to play games and deny disability insurance benefits, but thankfully a New Mexico Federal Judge made them pay disability benefits and attorney fees. The Plaintiff, Mr. Paul Chandhok, was recently awarded disability benefits in a decision by The United States District Court for the District of New Mexico, in a case decided on August 13, 2021. What makes this decision important for plaintif... Read More >

In Darren Mickell v. Bert Bell/Pete Rozelle NFL Players Retirement Plan (Plan), Mickell spent nine years in the NFL as a defensive end. He was repeatedly subjected to high speed contact hits which caused multiple orthopedic injuries to his “back, ribs, shoulders, arms, hands, knees, hips, legs, and feet." He had multiple orthopedic surgeries. Mickell also sustained multiple blows to his head t... Read More >

In Anne Ehlert v. Metropolitan Life Insurance Company (MetLife), Ehlert was a consulting pension actuary for pension plans at Towers Watson. Her first day of work with Towers was September 8, 2003. Her last day of work was December 23, 2015. In August 2016, she applied for long-term disability (LTD) benefits under her employer’s disability insurance benefit plan which was administered by MetLife.In thi... Read More >

They were very professional with their responds and on time with keeping you inform about everything with your case. I would recommend My lawyer Stephen Jessup, he was on point with everything, thank you. You guys are awesome people to work with. God bless you guys.

I was not able to work as a physician for about 14 months due to neck/back issues. Even though I had 3 medical doctors explicitly state that I was not to work AT ALL as a physician at that time, New York Life (NYL) Disability Insurance denied my long term disability claim (which apparently they deny a high percentage of people similar to me- only they know why they do this to so many- I have my own suspicions). I was in pain from my medical issues and so frustrated with NYL considering I had many bills coming due. I then decided to call Dell Disability Lawyers. One of their attorneys, Alex Palamara, spoke to me on the phone right then to hear and understand my story and then offer ways he could help. Long story short, within a few months of me returning back to work, he was able to persuade NYL to pay me my long term disability claim. He (and his kind assistant, Tabitha) were always very helpful, informative, and available to me. I feel quite certain that NYL would NEVER have paid me what was appropriate based on my insurance agreement/ contract with them without the help of Alex. I highly recommend him/Dell Disability Lawyers. If you find yourself in a similar situation of disability insurance denial of your own personal/group policy, especially if you are a medical provider/physician like me, then consider contacting them for advice/direction PRIOR to appealing your claim on your own.

Jay Symonds and his assistant, Sonia helped me tremendously. The insurance company that worked for my former employer did everything they could to make my life literally miserable. That all changed when I hired Jay. He and Sonia fought for my rights and forced the insurance company to pay what they should have.

If you have a disability claim hire Jay as if you go it alone the insurance company will screw you. Jay and Sonia will fight for everything you are entitled for. I couldn’t recommend them more highly.

I cannot say enough positive things about my experience with Dell Disability Lawyers. Attorney Stephen Jessup and Amanda offered an opportunity to provide clarity on a complex issue regarding my disability claim. Mr. Jessup offered advice on an offset to my claim after my insurance company asked for additional information from Social Security. With counsel from Mr. Jessup, I was able to address the outstanding issue with the Social Security office and provide my insurance company with the required documentation to address their concerns. Mr. Jessup always responded in a timely manner with expert advice and offered the opportunity for follow up. I strongly recommend Dell Disability Lawyers to those seeking legal counsel for disability matters.

I have been able to help others as a soldier, a police officer, and a pharmacist. I needed help forcing the insurance company to keep their commitment to take care of me and my family. I called Dell. Alex, Tabitha, and their entire team were very compassionate, extremely patient, and extraordinarily knowledgeable. Many thanks Dell!

My husband had applied for Long Term Disability and was denied. We sought out Rachel Alters at Dell Disability Lawyers to help us with our appeal. Rachel and her team were so diligent and meticulous in every aspect of the process. The process was seamless, and we never had any doubts that she would get it done and that she did! We are forever grateful to Rachel and Catherine for all of their determination and tenacity to get us the outcome we needed and deserved.

We could not recommend better representation and are indebted to them for making us whole again. Thank you so much Rachel and team!

Jam

Alex Palamara is one of The Best lawyers in the world and Dell Disability Lawyers are the Best by Far. Alex and his Assistant Tabitha helped me get the compensation I needed for a Horrific Disabling heath condition I’ve been dealing with for over a year. Alex and his team were so professional and caring. They treated me like I was there own family. Alex Knowledge, Expertise and skills as a Lawyer is among the Best of the Best in his field and I would HIGHLY recommend that if you ever have any issues with any Insurance Company over your Disability issues, please don’t hesitate to seek out Dell Disability and Alex Palamara. They truly are Amazing and caring. Thank God for them. Outstanding Job Alex and Tabitha

9 years ago when I had to apply for disability benefits from my private disability policy the insurance company ignored my inquiries until Dell and Schaefer represented me and I have received the benefits without interruption til my policy expired at age 65. I have appreciated not having to deal directly with the insurance company and having attorney Greg Dell and assistant Danielle Lauria handle all communications which included monthly progress reports. I thank them for their efforts on my behalf and highly recommend them to all those in need of disability benefits.

I’m so thankful I chose to reach out to the attorneys at Dell. They have always been quick to respond to any and all questions I have had. The anxiety I had while dealing with Lincoln Financial on my own has decreased immensely since Alex and Danielle took my case. They were able to get my LTD denial reversed and I am so very grateful!

Our goal is to get your application for disability insurance benefits approved. Applying for disability insurance benefits can be a difficult process and the information you provide is critical. Most disability insurance companies look at your application in hopes of finding a reason to deny your claim. Your disability company will ask you to complete numerous forms, interview you, request lots of information, speak with your doctors and possibly request to have you examined by their hired gun doctor.

Through our experience of having helped thousands of disability insurance claimants, our disability insurance lawyers will guide you through the entire application process and give you the best chance to get your disability claim approved the first time.

If your disability insurance benefits have been wrongfully denied, then our disability insurance lawyers know exactly what it takes to get your disability claim approved. You only get once chance to submit an Appeal, therefore every piece of evidence that will support your disability claim must be included. The goal is to win your disability benefits at the Appeal level, but while preparing your Appeal you must consider how a federal judge will review your disability claim if your benefit denial is upheld.

Preparing a strong disability appeal package is an art that requires you to understand how the courts interpret your disability policy language, ERISA regulations / laws, and how to strategically present evidence in support of your definition of disability. We encourage you to contact any of our long-term disability attorneys for a free immediate review of your disability denial.

98% of the disability insurance lawsuits filed by our law firm have resulted in either the payment of benefits or a lump-sum settlement agreement. Our disability insurance attorneys have filed ERISA governed and private policy long term disability insurance lawsuits against every major disability insurance company in state and federal courts nationwide and we love fighting for the little guy against the multi-billion dollar insurance company giants.

We have recovered hundreds of millions of dollars for our clients and we would like the opportunity to provide you with a free review of your disability benefit denial. There are many complex factors in a disability benefit lawsuit and the legal battle to win long term disability benefits can be fierce.

Approval of long-term disability is a continuous process as every disability insurance company will evaluate your eligibility for benefits on a monthly basis. You can never let your guard down and assume that your disability company will continue to pay your benefits for as long as you think you need them.

Our disability insurance law firm offers a reasonable flat fee monthly claim handling service in which we handle every aspect of your long-term disability claim and do whatever it takes to make sure you are paid every month.

Let's discuss if a lump-sum settlement or buyout of your disability insurance claim is both available and makes financial sense for you. Our disability insurance lawyers have negotiated more than five-hundred million dollars in disability insurance buyouts and we know how to get you a maximum settlement. A disability insurance company is not required to offer a buyout and not every disability company offers them.

We are disability insurance attorneys that know how to get your short or long term disability benefits paid. As a nationwide law firm we have helped thousands of disability insurance claimants throughout the United States to collect hundreds of millions of dollars of disability insurance benefits from every major disability insurance company.

Our attorneys have been able to either get our clients paid monthly disability benefits or obtain a one-time lump-sum settlement in more than 98% of our cases. Our disability insurance lawyers have seen it all when it comes to disability insurance claims and we know exactly what it takes for your disability claim to be approved.

We offer disability insurance attorney representation nationwide and we welcome you to contact any of our LTD lawyers for a free immediate review of your disability claim. We also invite you to visit and subscribe to our YouTube channel where we have more than 900 videos and regularly provide tips to help protect your disability benefits.

Who do you help?

Our disability insurance attorneys help individuals that have either purchased a long term disability insurance policy from an insurance company or obtained short or long term disability insurance coverage as a benefit from their employer. We have helped individuals in almost every type of occupation with monthly disability benefit payments ranging from $1,500 to $50,000.

Our clients include all types of employees ranging from retail associates, sales representatives, government employees, police officers, teachers, janitors, nurses, pilots, truck drivers, financial advisors, doctors, dentists, veterinarians, lawyers, consultants, IT professionals, engineers, professional athletes, business owners, and high level executives.

A strong understanding and presentation of the duties of your occupation is essential for securing disability insurance benefits.

Do you work in my state?

Yes. We are a national disability insurance law firm that is available to represent you regardless of where you live in the United States. We have partner lawyers in every state and we have filed lawsuits in most federal courts nationwide. Our disability insurance lawyers represent disability claimants at all stages of a claim for disability insurance benefits. There is nothing that our lawyers have not seen in the disability insurance world.

What are your fees?

Since we represent disability insurance claimants at different stages of a disability insurance claim we offer a variety of different fee options. We understand that claimants living on disability insurance benefits have a limited source of income; therefore we always try to work with the claimant to make our attorney fees as affordable as possible.

The three available fee options are a contingency fee agreement (no attorney fee or cost unless we make a recovery), hourly fee or fixed flat rate.

In every case we provide each client with a written fee agreement detailing the terms and conditions. We always offer a free initial phone consultation and we appreciate the opportunity to work with you in obtaining payment of your disability insurance benefits.

Do I have to come to your office to work with your law firm?

No. For purposes of efficiency and to reduce expenses for our clients we have found that 99% of our clients prefer to communicate via phone, email, fax, or video conferencing sessions. If you prefer an initial in-person meeting please let us know. A disability company will never require you to come to their office and similarly we are set up so that we handle your entire claim without the need for you to come to our office.

How can I contact you?

When you call us during normal business hours you will immediately speak with a disability insurance attorney. We can be reached at 800-698-9159 or by email. Lawyers and staff must return all client calls same day. Client emails are usually replied to within the same business day and seem to be the preferred and most efficient method of communication for most clients.