SAP America Solution Advisor Expert With Cervical Spondylosis Wins Michigan Hartford Long-Term Disability Insurance Appeal After Benefits Terminated by Internal Paper Review

Hartford terminated nearly two years of approved long-term disability benefits for an SAP America Solution Advisor Expert in Michigan — using an internal paper review by a non-physician who never examined our client, and invoking the any occupation disability standard months before the policy permitted it.

Our client spent close to three decades building one of the more exceptional careers in enterprise technology before cervical spondylosis with radiculopathy, secondary polycythemia, profound cognitive impairment, and related conditions made work impossible. Hartford’s response was to skip independent testing entirely, selectively quote favorable office notes, and hand off the vocational analysis to a process that was already predetermined. We have handled thousands of Hartford disability insurance claims and this approach is one we know well.

Disability insurance attorney Alexander Palamara assembled the objective evidence Hartford had declined to obtain, filed a comprehensive ERISA appeal, and Hartford reversed the termination in full — reinstating benefits for both own occupation and any occupation through the present.

What Palamara built in this appeal, and why it worked, holds direct lessons for anyone facing a Hartford denial. If The Hartford or any other disability insurance company has terminated your claim, speak with one of our disability insurance attorneys today. We represent claimants nationwide and charge no fee unless benefits are paid.

Table Of Contents

Why This Case Matters for Every Hartford Claimant

Hartford’s internal paper reviews are not independent evaluations — and a termination built on one is vulnerable. A paper review, also called a file review, occurs when an insurer’s own Medical Case Manager (MCM) evaluates your records from a desk without ever examining you, speaking with you, or consulting a specialist.

The MCM in this case concluded that “restrictions and limitations are not supported” — a finding drawn from selectively quoted notes while ignoring consistent documentation of decreased cervical range of motion, crepitus, and observed cognitive decline. That is not a medical conclusion. It is an administrative result written toward a predetermined outcome.

When the insurer won’t commission independent testing, you need to. Hartford had the contractual right to send our client to an independent medical exam, a Functional Capacity Evaluation, or a cognitive assessment — and chose not to. That left the record without objective functional data, which is exactly what a paper reviewer needs to support termination. We commissioned both a physical FCE and a Cognitive Functional Assessment. The results were devastating to Hartford’s position and left the insurer with nowhere to stand.

Applying the stricter “any occupation” standard before it is contractually due is a basis for appeal. Under most group long-term disability policies, the definition of disability changes at the 24-month mark — from inability to perform your own occupation to inability to perform any occupation for which you are qualified by education, training, or experience. Hartford applied this higher threshold months before the policy permitted, building a termination on a legal standard that had not yet taken effect.

Cognitive impairment that insurers ignore in the claim file can be proven with formal neuropsychological testing. Hartford’s own internal claim notes documented that during a phone call with our client, “his responses and attention span seemed to worsen the longer we talked.” Hartford performed no psychiatric evaluation, sought no neuropsychological assessment, and proceeded to a termination that assumed intact cognitive function.

Observable cognitive decline in a claim file does not prove disability — but formal testing with standardized, validated instruments, producing quantified and percentile-ranked scores, produces evidence that cannot be dismissed as subjective complaint.

A vocational analysis is only as credible as the medical foundation beneath it. Hartford’s Employability Analysis identified one occupation our client could allegedly perform — a high-level technology management role that demanded the same cognitive agility and technical precision his own job required.

When the medical basis for that conclusion is successfully challenged, the vocational output collapses with it. The only viable occupation Hartford could find was effectively the same job our client could no longer do.

How Cervical Spondylosis and Cognitive Decline Ended a 30-Year Career at SAP America

Our client served as a Solution Advisor Expert at SAP America, where he earned a base salary exceeding $150,000 plus substantial annual performance bonuses. His role was not sedentary in any functional sense. He was responsible for architecting enterprise-scale solutions for high-value clients, leading teams of up to 100 employees during large-scale initiatives, and serving as the authoritative technical resource in high-pressure, real-time client engagements.

Over nearly three decades, he accumulated more than 76 professional IT certifications, delivered keynote addresses at international conferences, and maintained a perfect success rate on digital transformation projects. Other directors and senior managers routinely relied on him to solve, on the spot, the problems no one else could.

What made his role uniquely demanding — and what the claim file systematically undervalued — was the cognitive load it required. His professional value resided not in his ability to sit at a desk but in his ability to retrieve vast stores of technical knowledge under pressure, synthesize complex system configurations in real time, and communicate precise solutions simultaneously to technical staff and senior executives. That capacity was what broke down first.

His medical history traces back to military service as an Air Force combat photographer, during which he sustained injuries in two helicopter crashes and a parachuting incident. Those traumas produced progressive cervical spine damage that worsened over decades. He underwent a three-level cervical fusion after losing motor control in his left arm, and, as degeneration continued, a seven-level cervical fusion with hardware removal. The recovery was severe and prolonged, marked by unrelenting pain, involuntary tremors, and gastrointestinal complications.

His full diagnostic picture, as established across the clinical record, included:

- Spondylosis with radiculopathy, cervical region (ICD-10: M47.12) — degeneration of cervical vertebrae compressing nerve roots, causing radiating pain, numbness, and weakness throughout the neck, arms, and upper back

- Spinal stenosis, cervical region (ICD-10: M48.02) — narrowing of the spinal canal placing sustained pressure on the spinal cord and nerve roots

- Post-laminectomy syndrome (ICD-10: M96.1) — a persistent pain syndrome following spinal surgery, compounded by multiple prior cervical procedures

- Secondary polycythemia and leukocytosis, BCR-ABL negative (ICD-10: D75.1) — abnormal overproduction of red and white blood cells requiring monthly therapeutic phlebotomies, bringing severe fatigue, diffuse body pain, rosacea, and elevated clotting risk

- Type 2 Diabetes Mellitus (ICD-10: E11.9) — diagnosed during the period of physical decline, adding to the overall medication burden

- Adjustment Disorder with Mixed Anxiety and Depressed Mood (ICD-10: F43.23) — documented by treating providers and confirmed during formal cognitive evaluation; Cymbalta prescribed by treating providers for both depression and neuropathic pain

- Chronic gastrointestinal dysfunction — including recurrent vomiting and diarrhea requiring eventual gallbladder removal, persistently disrupting medication absorption and daily function

The combination produced a daily reality nothing like the picture Hartford drew from isolated office notes. Pain regularly reached nine to nine and a half out of ten even on opioid therapy. Sleep was fragmented to four or five hours most nights, interrupted by severe pain, with full crashes into twelve to fourteen hours of recovery sleep recurring multiple times each week.

The cognitive “brain fog” that resulted — from the interaction of chronic pain, disrupted sleep, opioid side effects, and progressive neurological damage — had reduced a man who once recalled complex system configurations from memory to one who could no longer hold a conversation thread without it trailing off.

Treating providers documented this pattern consistently across more than eighteen months of clinical encounters. During a pain management appointment, our client himself stated that he did not believe he could return to any level of work, “not even sedentary, as he cannot concentrate and stay focused with the medicines he is on.”

Hartford’s Denial: A Desk Review, a Five-Day Ultimatum, and a Foregone Conclusion

Hartford’s termination was driven by an internal paper review conducted by its Medical Case Manager — a non-physician — reviewing only a small subset of provider records without speaking with or examining our client. The MCM concluded that our client was capable of full-time sedentary work, citing the most recent office visit in the claim file, during which he appeared without visible distress and certain exam findings were characterized as within normal limits.

This was selective to the point of distortion. The same visit also documented decreased cervical range of motion and ongoing medication titration. The MCM acknowledged the restricted neck movement but dismissed it because it was “not quantified.” Yet consistent documentation of restricted cervical rotation across more than a dozen separate clinical encounters over eighteen months constitutes clinical evidence — regardless of whether a number appears beside each finding.

Our client’s treating provider also explicitly noted lifetime restrictions and limitations in an Attending Physician Statement, reflecting the chronic nature of post-surgical cervical spine dysfunction. The MCM chose to disregard this as well, based on the absence of numerical measurements.

The process used to seek clarification from the treating provider was equally problematic. The MCM sent a validation letter demanding a response within five business days — explicitly stating that if no response was received within that window, a decision would be made on the existing file. The provider did not respond in time. Hartford finalized the termination on that basis, penalizing our client for a physician’s failure to meet an arbitrarily compressed deadline. This approach — issuing a short-window ultimatum and treating silence as medical concession — does not constitute a good-faith effort to develop a complete clinical record.

Hartford also failed entirely to address our client’s cognitive impairments, despite the fact that its own claim notes from an internal representative documented, following a phone call with our client, that “his responses and attention span seemed to worsen the longer we talked.”

Rather than treating this observation as a signal to pursue neuropsychological evaluation, Hartford moved forward with a termination that assumed intact cognitive function. No psychiatric evaluation was performed. No mental health expert was consulted. The diagnosis of depression, explicitly identified by a treating nurse practitioner in an Attending Physician Statement, went unaddressed.

Ability Analyst Davis Cox’s denial letter stated: “Since the medical information available to us in the claim file does not support a functional impairment from your own occupation, and you have the functional capacity to work in any occupation as defined in the policy, your claim has been terminated, and no benefits are payable beyond 3/31/2025.”

That conclusion — that our client could perform any occupation — was reached before the any-occupation standard was even contractually applicable. The policy’s 24-month own-occupation period had not yet expired at the time of termination, meaning Hartford applied the wrong legal standard to justify a benefit cutoff it was not yet entitled to make.

Anyone whose Hartford benefits have been terminated should verify the precise date their policy’s disability definition is scheduled to change — applying the stricter any-occupation standard before that contractual threshold is independently challengeable grounds for appeal.

The Evidence Hartford Chose Not to Gather — So We Did

When attorney Alexander Palamara evaluated this claim, the deficiencies were immediate and significant. Hartford had relied on an internal, non-independent paper review. It had obtained no FCE. It had ordered no cognitive or neuropsychological assessment. It had not consulted a specialist. And it had identified a single alternative occupation that required the same high-level cognitive and technical performance our client could no longer deliver.

The Hartford long-term disability insurance ERISA appeal attorney Palamara assembled did what Hartford had declined to do: it generated objective, independently verified functional evidence.

Under ERISA, an administrative appeal is the mandatory formal review process a claimant must exhaust before filing a lawsuit in federal court — and it is the only opportunity to introduce new evidence directly into the record before the case is closed to any further development.

A Functional Capacity Evaluation (FCE) is an objective, standardized assessment conducted by a qualified physical therapist that measures a person’s actual ability to perform work-related tasks over a sustained period, establishing their physical limits under validated testing conditions. We had our client undergo an FCE conducted by a licensed physical therapist with a Doctorate of Physical Therapy and certification as a work capacity evaluator.

We also commissioned a Cognitive Functional Assessment (CFA) — a comprehensive neuropsychological evaluation that measures cognitive abilities including memory, executive function, processing speed, and attention through standardized instruments, producing objective, percentile-ranked scores. This evaluation was conducted over two telehealth sessions by a licensed clinical psychologist with academic appointments at the doctoral level.

Both evaluations incorporated validity measures, confirming that our client’s performance reflected genuine functional impairment rather than exaggeration or effort problems.

The FCE: Below Sedentary on Every Relevant Measure

The FCE results established that our client could not perform sedentary work — the minimum physical demand category defined by the U.S. Department of Labor’s Dictionary of Occupational Titles — because he could not sustain the prolonged sitting it requires. Sedentary work, as defined by the DOL, requires the ability to sit for most of a workday, typically up to six hours. Key FCE findings included:

- Sitting tolerance: Occasional only — up to one-third of the workday in 25-minute increments; far below the six hours required for sedentary-classified occupations

- Static standing: Occasional, in 25-minute increments

- Walking tolerance: Occasional, in 15-minute increments

- High-level balance testing: Not passed; restricted from ladders, heights, and uneven surfaces due to dizziness

- Above-shoulder and above-eye-level work: Restricted due to limited cervical extension

- Prolonged neck positioning: Contraindicated due to increased cervical pain with sustained positioning

The licensed physical therapist concluded that our client was best suited for the Light physical demand category — not Sedentary — and specifically noted that “SEDENTARY work requires frequent sitting which client cannot tolerate.” She observed that our client’s previously reported position as Director of North American Tech Sales Support requires frequent sitting and that he would not be able to return to that role.

This finding directly contradicted Hartford’s Employability Analysis, which was built entirely on the MCM’s unsupported conclusion that our client was capable of full-time sedentary physical demand. The Employability Analysis defined sedentary work as requiring frequent handling and fingering, frequent arm extension at waist and desk level, and the ability to sit for extended periods — functional demands the FCE demonstrated our client objectively could not meet.

We have resolved prior Hartford appeals involving this same dynamic, including a Hartford LTD appeal won for a computer systems administrator with chronic back pain and an ERISA appeal victory where FCE evidence reversed a Hartford termination.

The Cognitive Assessment: Scores That Erased What Remained of Hartford’s Position

The Cognitive Functional Assessment results were equally unambiguous — and in some respects, more striking.

To understand the significance of these scores, context matters. Our client’s premorbid intellectual functioning was almost certainly in the high-average range. Decades of elite technical performance, 76 professional certifications, keynote presentations at international conferences, and leadership of enterprise-level digital transformation initiatives do not occur at average cognitive capacity. What the formal testing found was not baseline limitation. It was collapse.

Key results from the standardized evaluation included:

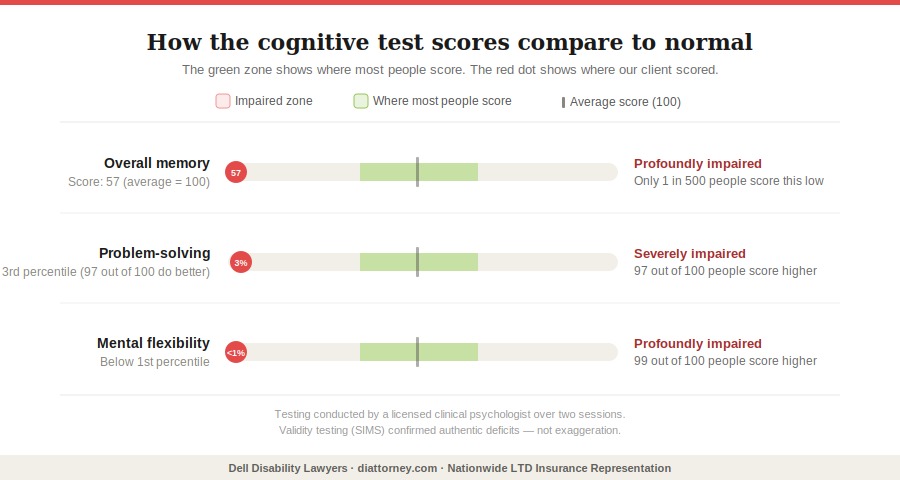

- Composite Memory Index (CMX): 57 — profoundly impaired range; this score represents overall memory function across verbal and nonverbal domains

- Nonverbal memory: score of 20 — profoundly impaired; inability to retain and recall non-verbal information such as spatial patterns, visual sequences, or diagrams

- Working memory: severely compromised — significant difficulty holding and manipulating information in real time, which underlies every analytical or technical task

- Verbal memory: score of 37 — below expected levels given premorbid functioning; difficulty recalling verbally presented material

- Executive function (Wisconsin Card Sorting Test) — Total Errors: 3rd percentile — substantial difficulty with accurate problem-solving and adapting to changing conditions

- Conceptual Level Responses score: below the 1st percentile — severe deficit in cognitive flexibility and the capacity to identify and apply new strategies when circumstances change

- Perseverative responses: borderline impaired — tendency to continue applying an ineffective approach even after feedback indicates a rule has changed

What these numbers mean in practice: our client could not reliably store information presented to him during a task and retrieve it minutes later. He could not adapt when a problem shifted. He could not sustain the pace, accuracy, or reliability that any competitive workplace demands. The clinical psychologist noted that these depressed results were produced under conditions of severe pain — rated at nine and a half out of ten during the second session — and following a night without sleep due to gastrointestinal distress, meaning the true impairment was, if anything, understated.

The Structured Inventory of Malingered Symptomatology (SIMS), a validated instrument specifically designed to detect exaggeration of symptoms, returned negative findings. These were authentic deficits.

The assessment also included a functional capacity rating table across occupational dimensions. Our client was rated at Severe Impairment on the ability to switch between tasks, concentrate and maintain pace, and complete a normal workday without interruption from physical or cognitive symptoms. He was rated at Moderate Impairment on the ability to maintain a conversation topic, remember important tasks, learn new tasks, follow detailed instructions, make simple work-related decisions, and deal with normative occupational stress. He retained Mild Impairment only on the ability to interact socially.

For a claimant whose occupation required precisely the ability to switch between complex tasks, sustain pace under pressure, and maintain performance across long and demanding client engagements — these findings were not supplementary. They were definitional.

The clinical psychologist’s conclusion was direct: while verbal reasoning remained relatively preserved, it could not compensate for profound deficits in memory, processing speed, and executive functioning, making it impossible to sustain competitive employment including sedentary desk-based work. For additional context on how cognitive testing functions in Hartford disability claims, see our discussion of Hartford cognitive impairment appeals and the role of neuropsychological evidence.

The Vocational Conclusion: When the Only Available Job Is the Same Job

Hartford’s Employability Analysis, built entirely on the MCM’s paper review, identified exactly one occupation our client could allegedly perform: Manager, Computer Operations, at a monthly wage of $15,059.20.

That position was selected because it was the only role that met the policy’s earnings threshold — 60 percent of indexed pre-disability earnings, equivalent to approximately $10,443.60 per month or $60.25 per hour. Under Hartford’s own policy language, to disqualify our client from benefits under the any-occupation definition, the insurer needed to identify work he could actually do that met that earnings threshold.

The only work Hartford could find for a Solution Advisor Expert with nearly three decades of elite enterprise technology experience was a high-level technology management role. Think about what that actually means. A Manager, Computer Operations requires uninterrupted attention, rapid technical decision-making, detailed technical knowledge, and consistent cognitive communication under pressure.

Those are precisely the demands our client could no longer meet — the same demands that had made his own position untenable. The gap between “able to perform any occupation” and “able to perform only this single cognitively demanding technology management role” is not a gap at all.

This is a pattern worth watching for in Hartford disability benefit denials and how to prevent the most common termination tactics. When an insurer’s vocational analysis produces a single viable occupation — particularly one requiring the same skills as the claimant’s prior position — that analysis is built on an unstable foundation and is susceptible to challenge.

The Employee Retirement Income Security Act of 1974 (ERISA), under 29 U.S.C. § 1132, requires plan administrators to conduct a full and fair review of each claim. A vocational analysis predicated on a non-physician’s desk review, applied under the wrong disability standard, to a claimant for whom objective testing established the inability to perform even sedentary work, does not meet that standard.

Hartford Reverses in Full

Attorney Palamara submitted the appeal with the FCE report, the Cognitive Functional Assessment, updated treating provider records, and a comprehensive legal argument addressing every dimension of Hartford’s procedural and substantive failures — including the premature application of the any-occupation standard, the internally conducted paper review’s inadequacy as a basis for termination, and the vocational analysis that was only as credible as the flawed MCM conclusion underlying it.

As attorney Palamara wrote in the appeal, Hartford’s decision was “not only wrong, but also arbitrary and capricious” — based on a biased internal review conducted without independent examination, that ignored treating provider opinions, imposed an unreasonable deadline for a provider response, and built a vocational conclusion with no real-world credibility.

Hartford’s Appeal Specialist Joseph Simeone reviewed the complete record and reversed the termination. The reinstatement letter confirmed: “The decision to terminate is overturned from 04/01/2025 to Present” and that “the medical information supports Disability from Own Occupation and Any Occupation from 04/01/2025 to Present.”

Not just own occupation. Both definitions of disability. Hartford reinstated LTD benefits for our client, effective from the date of termination and covering both own occupation and any occupation definitions of disability. Our client remains on claim.

If Hartford Has Denied or Terminated Your Claim, Act Now

Under ERISA, 29 U.S.C. § 1133, claimants typically have 180 days from the date of a denial to file a formal administrative appeal. Missing that deadline can permanently extinguish the right to benefits and the right to sue. If the appeal is denied, a Hartford long-term disability lawsuit in federal court is the next available step. That clock does not pause while you search for representation.

The reality is that Hartford’s internal review process is built to reach a conclusion, not to discover one. When the MCM who never met our client can declare restrictions unsupported, and when a vocational analyst can identify one viable job that happens to require the same skills as the occupation our client left, and when all of that can be assembled in a denial letter — the only effective response is objective evidence that cannot be argued around. That is what this appeal provided.

If The Hartford or any other disability insurance company has denied or terminated your long-term disability benefits, contact our office today for a free consultation. Our disability insurance attorneys represent claimants in all 50 states. We have been fighting for disability claimants since 1979, we have helped tens of thousands of claimants collect more than $2 billion in disability insurance benefits, and we charge no fee unless your benefits are won.